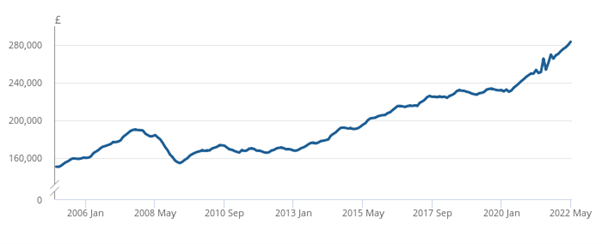

House prices have grown significantly over the last two years

Interest rates have been at an all-time low over the last two years. Post-pandemic work dynamics have incentivised people to move out of the larger cities into the country where they could afford houses and get more space. Result: the demand trumped supply, pushing house prices.

The average UK house price increased to £283,000 in May 2022

Source: HM Land Registry, Registers of Scotland, Land and Property Services Northern Ireland, Office for National Statistics – UK House Price Index.

There are signs that the market is slowing down.

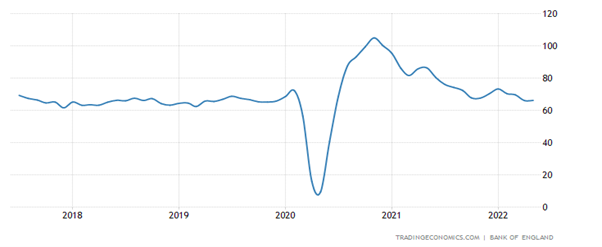

There are signs that the market is slowing down; some think this may be a sign of the times to come. Analysis of market data and statistics may help build a data-driven market view. As per the Bank of England, mortgage approvals have fallen from 69,000 in March 2022 to 66,000 in June 2022. While house prices are still rising, they expect the demand to weaken, causing prices to stabilise or fall. From May 2022 to June 2022, Nationwide’s data showed that annual house price growth fell by 0.5% to 10.7%, from 11.2%.

Mortgage rate approvals by the Bank of England

Though, it doesn’t mean a bad thing for property investors.

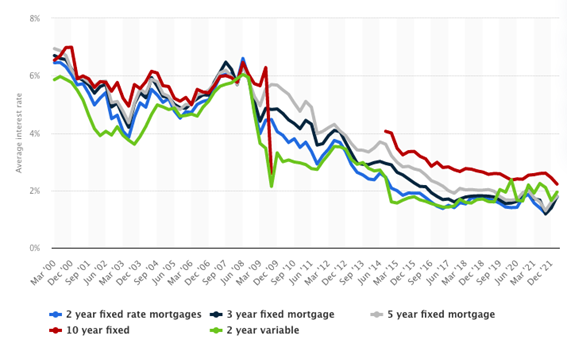

Yes, the interest rates are estimated to go up, but borrowing money is still relatively cheap when you compare today’s borrowing rates to those in 2012 or 2013. Rising rates will undoubtedly impact buyer sentiment and affordability and can potentially put many people off from buying properties, causing house prices to dip. But for many, this may be an opportunity to grab their dream property.

Average mortgage interest rates in the UK from March 2000 to February 2022

There is a possibility that a lot of inventory returns to the market as many investors exiting their two-year or five-year fixed mortgage period may feel the squeeze on their profits. Higher living costs, including food, energy, fuel, and taxes, are also not helping with the same.

Property investors are already thinking about holiday lets.

Growth in the holiday let sector and increased pressure on profits are already causing many investors to switch their investing strategy from BTL to holiday lets. As per BBC analysis of council figures, the number of holiday lets in England has risen by 40% in three years. Much of that growth has happened in areas with large numbers of such existing properties – including Scarborough, the Isle of Wight, North Devon, the Cotswolds and Norfolk.

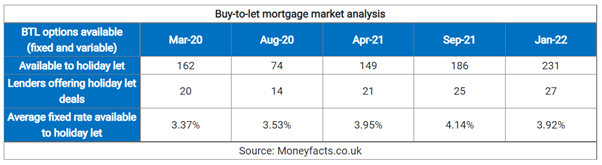

Wider acceptability of holiday mortgages among lenders is causing rates to fall, countering the overall rate hikes.

As of Jan 2022, there were 27 lenders offering 231 holiday-let mortgage products, up from 14 lenders offering 74 mortgage products in Aug-2020. This highlights the fact that lenders have increasingly become comfortable with this asset class. This is further supported by the evidence that the average fixed rate on the mortgages reduced to 3.92% in Jan-2022 from 4.14% in Sep-2021.

Property prices in the holiday let areas can be more resilient

Prices in London are still the highest in the UK, sitting at £520,000 on average. On the other hand, locations such as North Devon, Scarborough and East Sussex have seen some of the most significant growth, with all three areas have risen at three times the national average!

It’s still early to think a crash is coming, though holiday lets can be a natural hedge.

No signs suggest that property prices will “burst” or “crash” hard, as there is still significant interest in property investment, particularly in second homes. Further data is required to see if this decline in growth is a trend. However, property prices will likely become more reasonable, flipping it from a sellers’ market to buyers’ market. Recently, properties across the country sold significantly over their asking price, with a large proportion selling for 10% more than the asking price! But this is expected to come to an end soon.

An independent financial agent should thoroughly analyse your finances and your long-term goals to advise on the best investment time for you, as there is certainly no right or wrong time!